Zombie Hunt - UK Chapter

Zombie Hunt - UK Chapter

If they are there, they are hiding out extremely well

We know they’re out there: those companies undead only because zero interest rates kept them alive, feasting on valuable resources, sucking the life out of the nation’s productivity. Any economy where the time value of money sank to near zero for any length of time was their breeding ground. That means the US, the UK, the EU, Japan.

We’re talking zombies:

Now interest rates have risen, are we going to find the economic ground piled high with their finally-dead corpses? How many unwitting people will find themselves thrown out of work, the zombies last victims?

My working assumption has been that zero/near zero interest rates must have left Britain, the EU and the US hosting a . . . well, a host of zombies. But as employment totals stay surprisingly buoyant even 18 months after rates started to rise in the US and UK, and nine months after rises started in the Eurozone, how long should we wait before we begin to see the zombie apocalypse?

How long should we wait before we conclude, reluctantly, that maybe there are a whole load of post-zombie companies out there, unable to grow, unable to die?

Let’s start by looking at the UK.

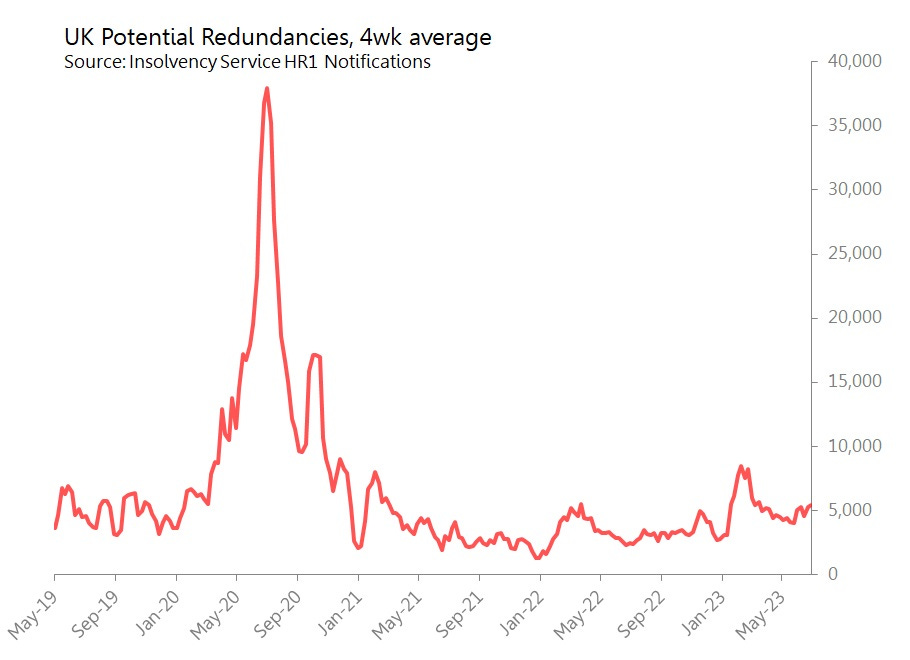

Labour markets are generally lagging indicators, but we have a lead indicator for that lagging indicator: any company intending to make more than 20 redundancies in the near future is obliged to submit their proposal to the Insolvency Service via the HR1 form. The ONS publishes these tallies on a bi-weekly basis, and currently the latest data is for the week to July 9th. As the chart shows, whilst there was a major surge in redundancies in 2020, this exhausted itself by 2Q21, and numbers have remained at low levels ever since. There is no sign here of an approaching tsunami of redundancies.

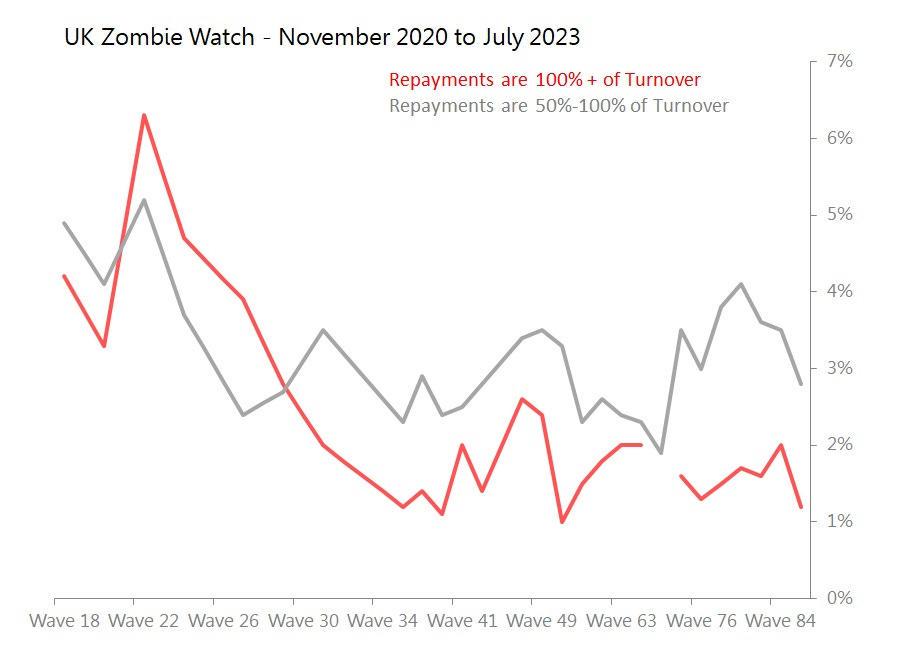

Why? The ONS also publishes a huge survey of corporate conditions on a regular basis, in which it asks slightly fewer than 39k companies about everything from turnover, pricing, profits, employment, capex and, of course, their financial condition. One of the questions essentially asks zombies to identify themselves: ‘Are your debt repayments equivalent to 100% or more of your turnover?’

At the peak in 2020, more than 6% of those responding confessed that this was the case - that the debt repayments they must make exceeded their annual turnover. A further 5% reported that they were potential zombies, with debt repayments were between 50%-100% of turnover.

But the situation has changed and improved dramatically since then. In the latest survey (June), only 1.2% of companies reported themselves at the 100%+ level, and only a further 2.8% at the 50%-100%.

The message it sends is: ‘No zombies here’.

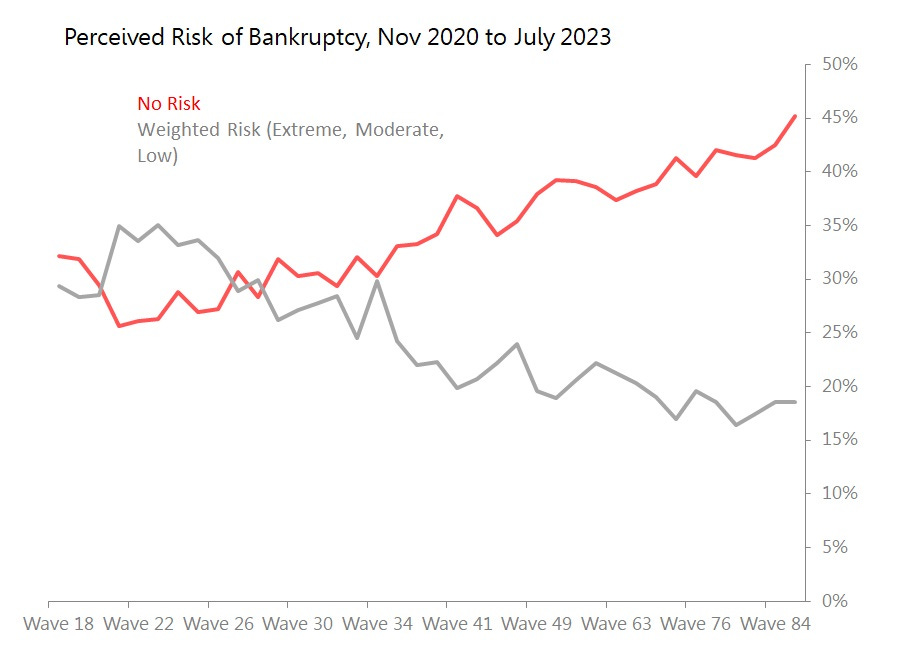

The same survey directly asks companies to assess their chances of insolvency in the near term, with possible answers include: ‘severe risk’, ‘moderate risk’, ‘low risk’, ‘already insolvent’ and ‘not sure’. The latest results have ‘severe risk’ at 1%, ‘moderate risk’ at 8.3%, ‘low risk’ at 33%, ‘no risk’ at 45.2%, ‘already insolvent’ at 1% and ‘not sure’ at 11.4%.

The chart below generates a weighted risk, with weightings of 2 for ‘severe risk’, 1 for ‘moderate risk’ and 0.25 for ‘low risk’. On those weightings, the self-perceived risk of business failure dwindled almost continuously from 2020 until bottoming out at low levels since February 2023. Meanwhile, the proportion of companies seeing ‘no risk’ of bankruptcy rose from a low of around 25% in late 2020 to around 45% now.

The message seems to be that if the UK economy is harbouring a dangerous throng of zombies about to be pole-axed by rising interest rates, they are hiding very effectively.

This echoes what I found looking at UK Kalecki profits, return on capital directional indicator and private cashflows in my June 12th piece ‘UK Economy: SNAFU vs Catastrophe’. Those metrics were surprisingly good.

It concluded: “None of these relatively positive signals and ratios guarantees that the UK economy will not be hit by a catastrophic crisis of confidence. It is difficult to identify the urgent or emerging crisis in key economic stocks needed to generate a catastrophic response in economic or financial flows.

“This relatively relaxed conclusion does not mean Britain’s fundamental economic policies are good. They are not: they are very actively inhibiting growth, productivity, maintaining key national infrastructures, and effective public administration. Moreover, for decades, public policy has played a key part in generating some of most extreme regional inequalities in any developed country.

“In many ways, Britain’s economy ought to be failing, ought to be courting catastrophe. But it isn’t.”

Similarly, Britain’s economy ought to be facing an impending zombie apocalypse. But so far as we can tell, it isn’t.

Yes, I'm obviously going to have to explore more. The data seems to suggest that a few zombies got the stake through the heart in 2020, but died very quietly under the medically-induced economic coma, with BOE/Govt being discreet undertakers. It also suggests, more widely, that large parts of the private sector used the pandemic's largesse to reconstruct personal and corporate balance sheets.

So more work to do. But the question in my mind is: 'why are our mainstream media so useless/incurious about all this stuff. It shouldn't be left to someone living thousands of miles away and actually having a full-time job, to explore this stuff. Pathetic!

This is fascinating Michael, as I did not know about this survey.

The obvious question is why the Zombies haven't emerged in a highly leveraged economy that has seen a sharp rise in interest rates. I see two narratives. Have exploitive British businesses pushed price increases onto long-suffering consumers who run up more debts to keep spending? Or do we have two economies in Britain, with a moribund state monopoly and a dynamic entrepreneurial community passing each other like ships in the night.

No doubt this is a false dichotomy, but is the answer something you have or will be writing about?