UK Economy: SNAFU vs Catastrophe

Policy and administrative failure has not yet completely killed the economy

How much punishment can the UK economy take before catastrophe overtakes it? The UK government pursues a broad swathe of growth-inhibiting policies, made worse by a civil service which, unable to increase the supply of public goods, concentrates on fining, banning and pricing away public demand. Meanwhile, for decades public policy has been complicit in stretching regional inequalities so widely that it is doubtful whether the UK remains a ‘coherent sample’.

Twice in the last week, I found myself listening/reading to economists catastrophising about the UK economy, specifically prophesying the collapse of sterling and a run-away spiral in UK interest rates. My gut instinct is that when catastrophising becomes mainstream, it’s probably time to start buying (in this case, sterling and long gilts).

But am I right?

Much of the disaster-scaping extrapolates from the UK’s anomalous CPI results and deteriorating fiscal position. But both these problems are the result less of generalized economic mismangement, than of specific malign policies which can, should, and perhaps partially are, being reversed.

The UK’s anomalous headline inflation is above all generated by an energy-pricing policy which dictates a) that consumer must pay at a cost equal to the highest marginal producers’ price; and b) that those prices can be re-set only very slowly. It is true that the damage of this ludicrous policy is rippling through to the broader set prices, as expected as a second-phase reaction to a energy-price shock. It seems unlikely, however, that Britain’s labour is sufficiently organized and/or unionized to trigger the third-phase - the feared wage/price spiral.

The second specific policy error is the inexplicably stupid decision to get Bank of England to finance pandemic-related debt with short term money, with the Treasury issuing an indemnity for all the losses such a position will generate. The Bank of England has previously estimated that this financing blunder will ultimately cost the taxpayer about £200bn. If so, it is the single biggest financial blunder in British government history. The chancellor at the time was Rishi Sunak, who is now Prime Minister.

How much has this cost so far?

The bills for the indemnity are now coming due: it cost £4.2bn in January, £5bn in March and £9.8bn in April. During the first four months of the year, Britain’s public sector net borrowing cam to £48.4bn, and the indemnity alone accounted for £19bn of that - ie, 39% of the deficit. That’s how much we’re already paying for the Treasury’s inexplicable funding blunder.

As for current spending (includes interest payments, but not capital spending, or the BOE indemnity, there’s a deficit of just £822mn.

If the UK’s most visible economic problems are directly the result of catastrophic public policy blunders, the good news is that their impact will moderate over time. Energy prices will be fixed at sharply lower levels in July and October, and this will immediately cut CPI. As for the Bank of England indemnity, it is not beyond the bounds of possibilities that Bank of England could use the money it is receiving to lengthen the maturity profile of its gilts holdings. If so, it remains possible that at some stage the holdings may even turn a profit for the taxpayer (don’t hold your breath, though).

The horrible energy and public sector funding errors are not the only problems the UK economy faces. But they are the two which form the foundations for the catastrophists prophecies. Apart from those, how immediate are Britain’s economic and financial problems? Spoiler alert: it all looks pretty ‘SNFU normal’.

Let’s take a look.

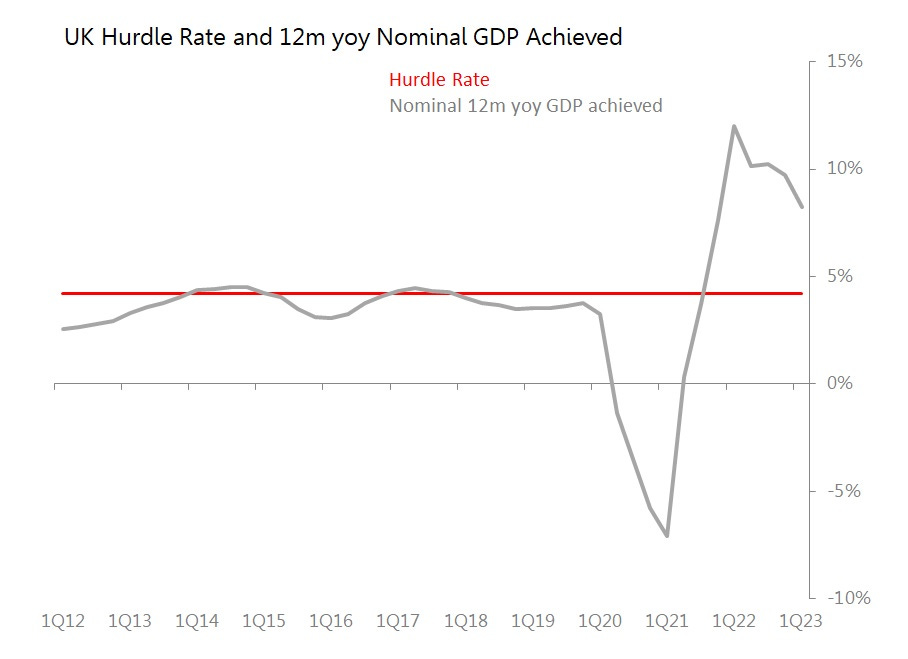

Public Debt - Bad but Sustainable

Using the same methodology I developed to establish a nominal GDP ‘hurdle rate’ below which interest payments alone would raise public debt/GDP levels, the UK position even now remains tolerable. Historically, the UK has typically achieved the sort of nominal GDP growth rates - even during this period of sustained low productivity growth - which would have allowed the current levels of public debt and current 10yr bond rates to be serviced essentially indefinitely.

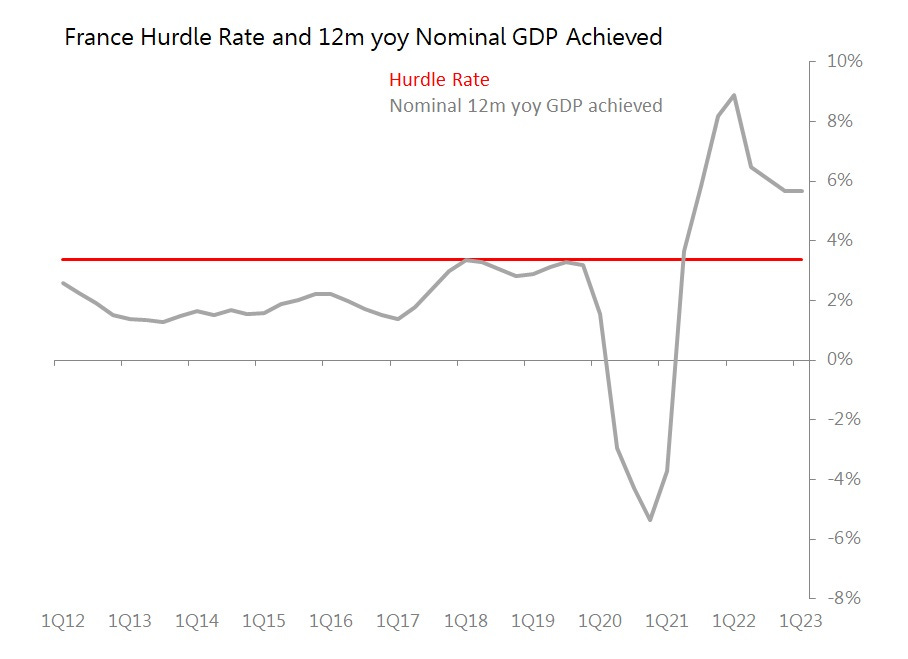

This is not something one can claim for a number of major European economies. France, for example, has rarely sustained its current hurdle rate:

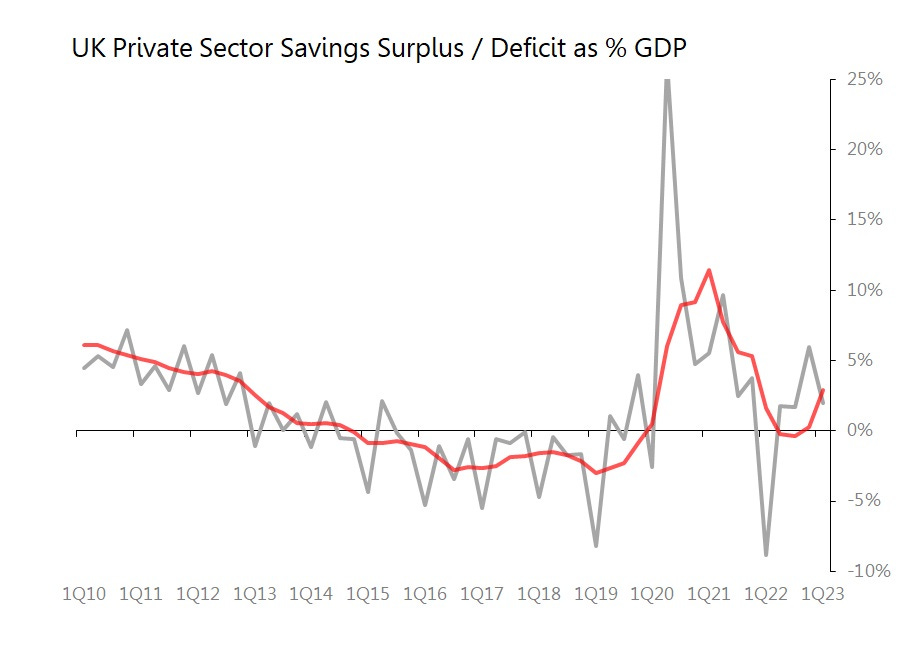

Private Cashflows - Modestly Positive

Then we need to look at the cashflows in the economy. The private sector continues to generate a savings surplus, which implies a positive cashflow between the private sector and the financial system. (Caveat: the Office for National Statistics regularly springs major revisions in Britain’s trade and current account data, and this introduces uncertainties to this measure.) However, in 2022, it seems the UK’s private sector had a flow of surplus savings equivalent to 0.3% of GDP (despite a huge deficit in 1Q22). Initial estimate of for 1Q shows that 12m surplus rising to around 2.9% of GDP.

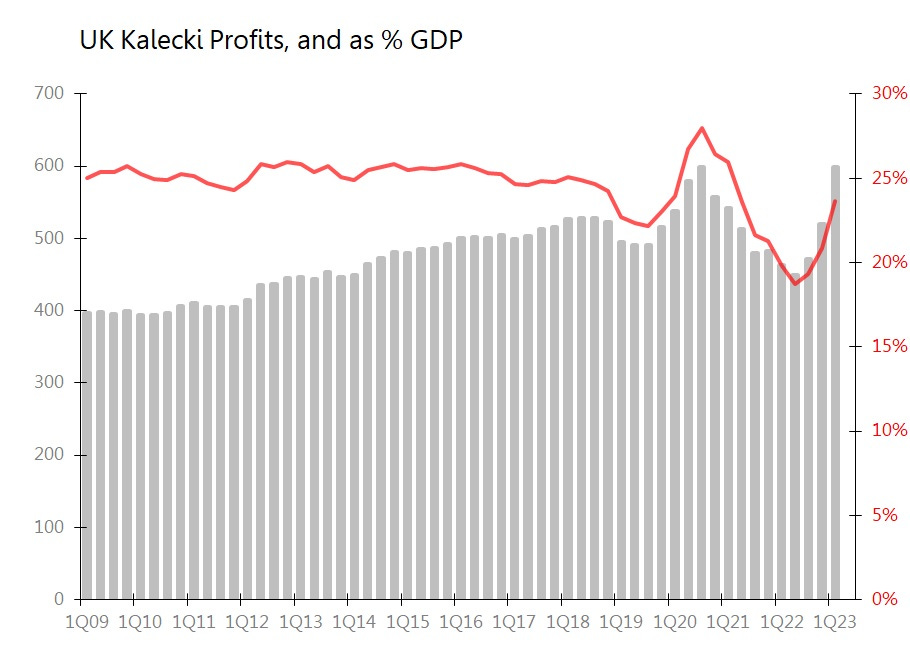

Kalecki Profits - Rising

I suspect these savings are concentrated in the corporate sector, where Kalecki profits rose 7.6% yoy in 2022, and accelerated to 29.3% yoy in the 12m to 1Q23. Profits as a % of GDP recovered to pre-pandemic levels.

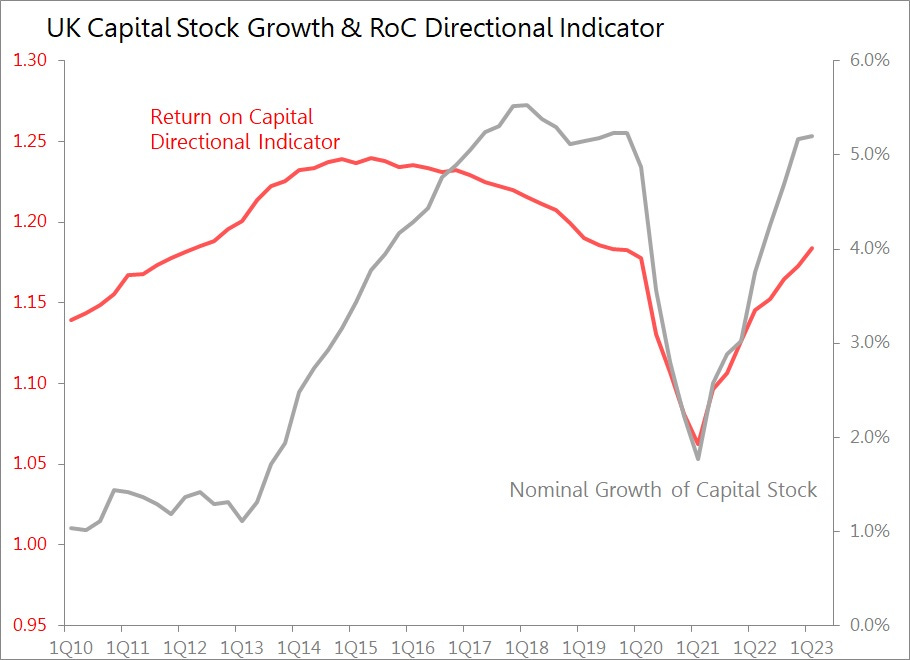

Return on Capital Directional Indicator - Still in Recovery

Similarly, the rather simple asset-turns proxy, which expresses final spending on domestic product (ie, GDP less inventories) as an income from estimated capital stock, continues to rise. It has recovered to pre-covid levels, but has some way to go to recover the peaks seen in 2014-2017. Nominal growth of capital stock, at just over 5% has just about reached its pre-covid peak growth levels. Growth in capital stock is peaking, but the continuing rise in ROCDI means a sharp fall is unlikely at this stage.

Cashflows and Leverage

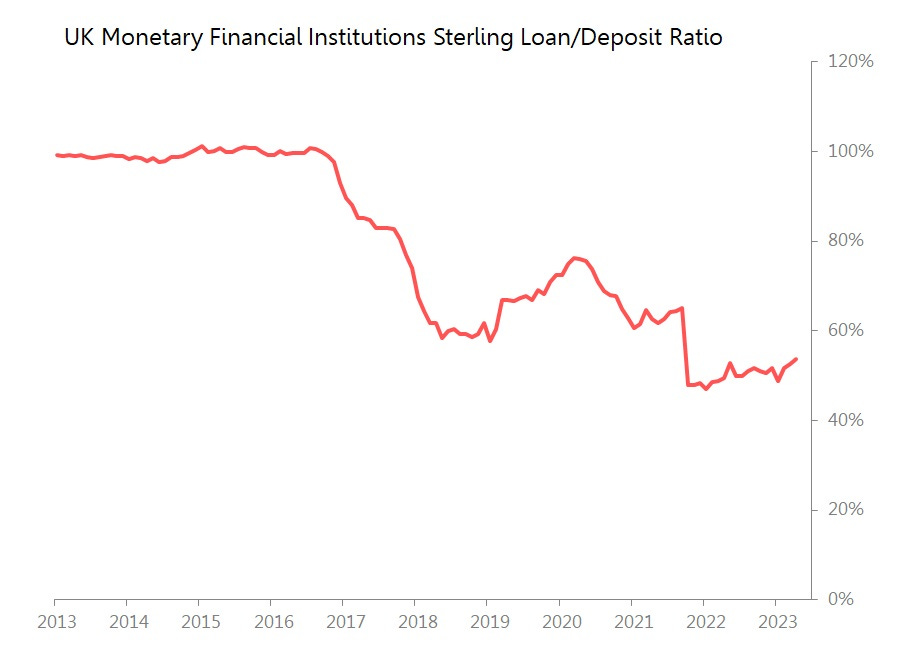

The positive net flow of private savings into the financial system implies there is no irresistible pressure for the banking system to provide sufficient net lending to allow current levels an patterns of economic activity to be maintained. Consequently, one would not expect the UK banking system to be highly leveraged in terms of loan/deposit ratios.

Although London’s role as a financial centre makes it difficult to extract the data with great certainty, it seems the loan to deposit ratio for sterling assets and liabilities for all monetary financial institutions monitored by Bank of England is currently below 60%. If so, it is no surprise that the UK banking sector has so far survived the rise in interest rates without significant stress. (Once again, the contrast with the Eurozone’s banks may be relevant: at April, Eurozone banks’ loan/deposit ratio was running at 93%).

Conclusion

None of these relatively positive signals and ratios guarantees that the UK economy will not be hit by a catastrophic crisis of confidence. It is difficult to identify the urgent or emerging crisis in key economic stocks needed to generate a catastrophic response in economic or financial flows. An incoming Labour government might try to to depth-charge the economy by even-more-aggressively growth-inhibiting policies. But with Sue Gray perched on Keir Starmer’s shoulder, it must be very doubtful that any significant change in Establishment policy will be permitted

This relatively relaxed conclusion does not mean Britain’s fundamental economic policies are good. They are not: they are very actively inhibiting growth, productivity, maintaining key national infrastructures, and effective public administration. Moreover, for decades, public policy has played a key part in generating some of most extreme regional inequalities in any developed country.

In many ways, Britain’s economy ought to be failing, ought to be courting catastrophe. But it isn’t. If this seems mysterious, it may be that currently analysts are blind to strengths emerging far from the normal radar of established expectations. For instance, every casual observer knows that Britain’s industrial base has disappeared. . .