US - A Cycle Ends, A Transition is Made, A New Cycle Emerges

This piece argues that the US's current cycle is ending, but transitioning into a new one . . . without recession. Not a modishly 'controversial' view, but rather one forced on me by the evidence.

OK, this one’s going to hurt: one way or another, some of my most cherished axioms or beliefs will have to fall.

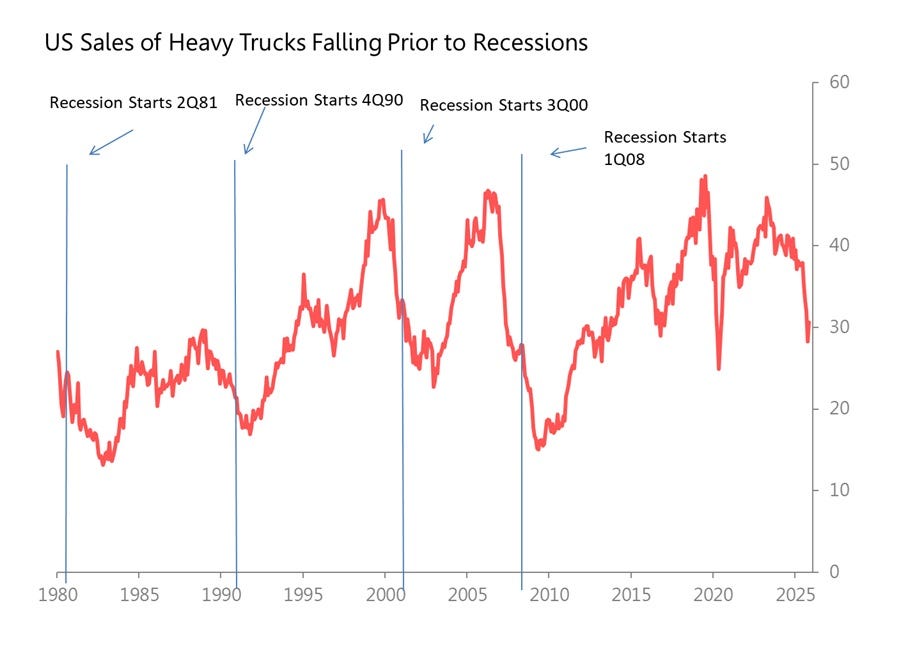

Here’s the problem. The most reliable early-indicator of an oncoming US recession has been a sudden fall in heavy truck sales. Unlike other so-called recession indicators (yield curve, I’m looking at you), this one hasn’t predicted seven of the last three recessions. It has predicted four of the last four recessions since 1980, or five of the last five if you count the impact of the pandemic. It has never been wrong, and (belatedly released) October data found sales down 26.9% yoy, on a 11.5% mom drop which was 2.5SDs below trend. That is precisely the sort of drop which turns the lights flashing red.

But here’s the problem: my other axiomatic belief is that recessions happen precisely when problems of stock (too much credit, housing or inventory overhang, fiscal meltdown etc) become so urgent that they have to be answered by a change (slowdown) in flows. It is that slowdown in flows which makes the recession, which is the recession, actually. But where’s the urgent stock problem? It’s showing up precisely nowhere in the available US data. It’s not showing up in credit growth or a crisis of credit quality, it’s not showing up in inventory overhangs, it’s not showing up in housing overhangs, and its not showing up in macro-investment totals. It’s not showing up in return on capital or Kalecki profits. Where there is obvious excess is the build-out of data-centres as the world’s deepest pocketed companies (and, separately, OpenAI) see an IA world coming into focus. They may be wrong, but the bets won’t bankrupt Microsoft, Meta, Elon etc). But whatever AI is, it ain’t tulips.

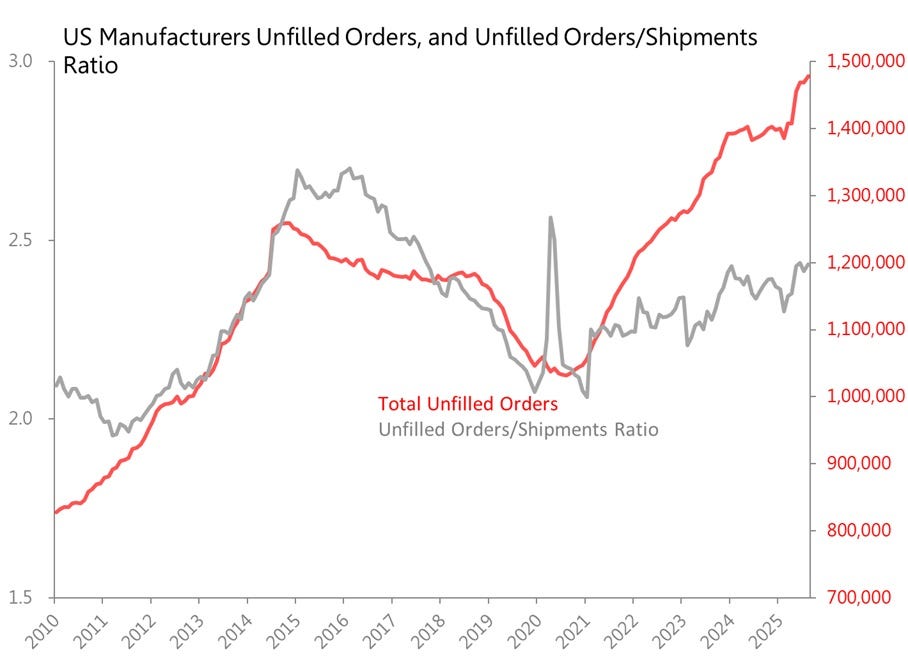

To give just one example of where a stock problem isn’t showing up, consider what’s happening in manufacturing backlogs. In September, backlogs were up 7% yoy and had never been higher. Are those totals flattered by inflation? Perhaps: but the backlogs/shipments ratio cancels out inflation’s impact, and in September that ratio was the highest seen since mid-2017 (except for the anomaly at the onset of pandemic-panic). I suppose it’s possible that an industrial recession might somehow emerge despite these conditions, but I’d say it was extremely unlikely.

Although the ISM’s manufacturing index, which is the grandfather of all PMIs and still the best, has come in under 50 for the last nine months, if you look at the details, you’ll find that customers inventories have been coming at under 50 (’too low’) for 14 months now. If there is a supply crisis in the US industrial sector, it’s not oversupply, if anything it is the reverse.

Which treasured truth have I to discard? They can’t both be right, so one of them will be proved wrong. Which?

My instinct tells me that it’s the heavy truck sales story that will prove false this time. Though not, perhaps, entirely. I do not think that the US is headed for recession because I don’t just can’t see the stock problem. But maybe if not a recession, maybe the US is headed into something very unusual - a period of unusually restrained growth which may or may not be rescued by fiscal, monetary and supply-side initiatives. What, perhaps, we are seeing is something very unusual, cyclical enfeeblement as a result of sustained inanition. The vigour of the cycle, if not the cycle itself, is dying of . . . of lack.

I haven’t seen it before.

Dying of Lack

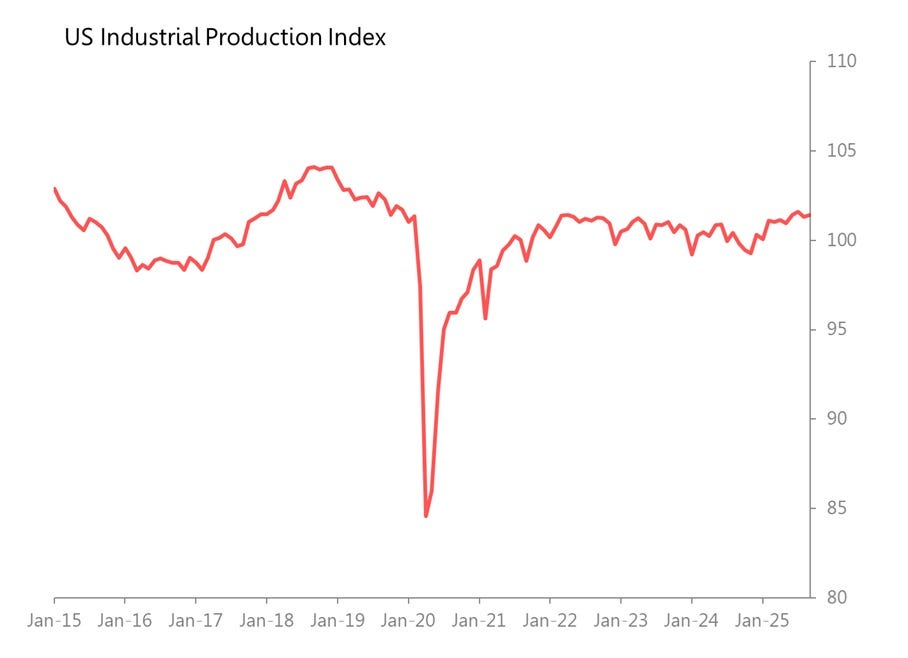

“Dying of lack.” What does it mean? Well, here’s industrial production - there’s no crisis, no disaster showing up in the chart, just essentially a flatline since 2022.

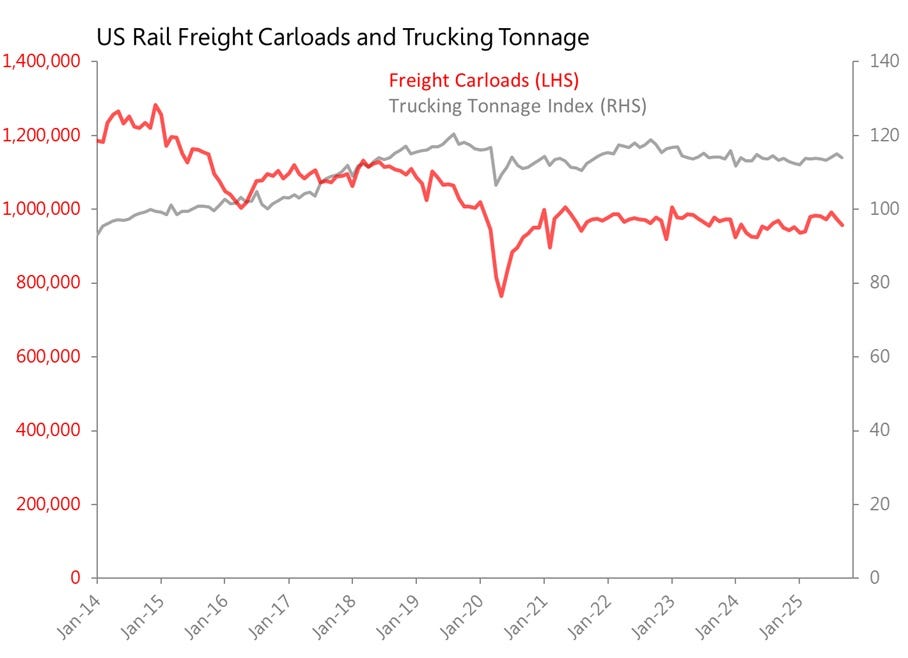

It is the same story, of course, for freight volumes: flatlining since 2021/2022.

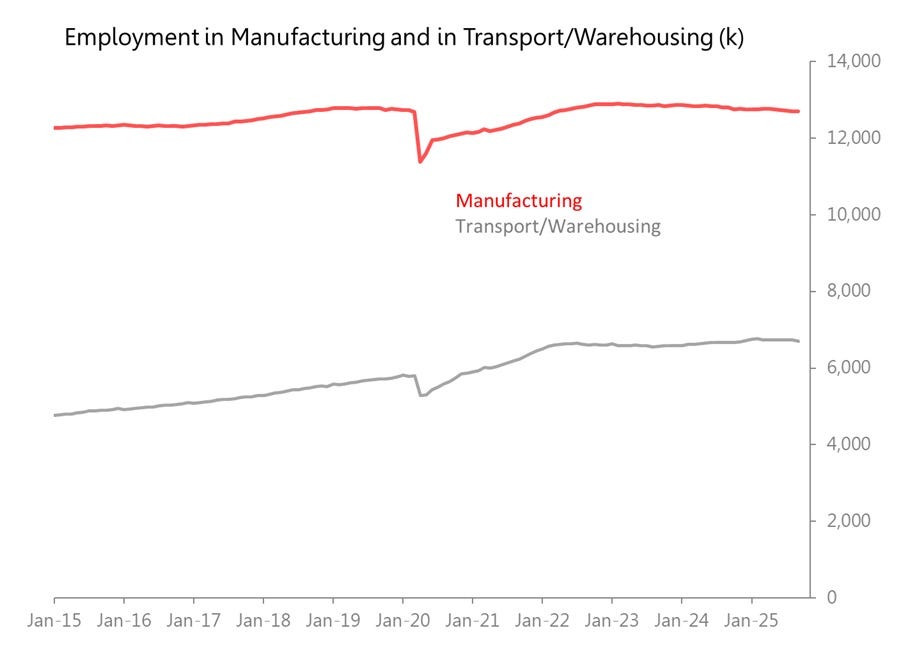

And this lack of positive impetus of course gets carried over to employment:

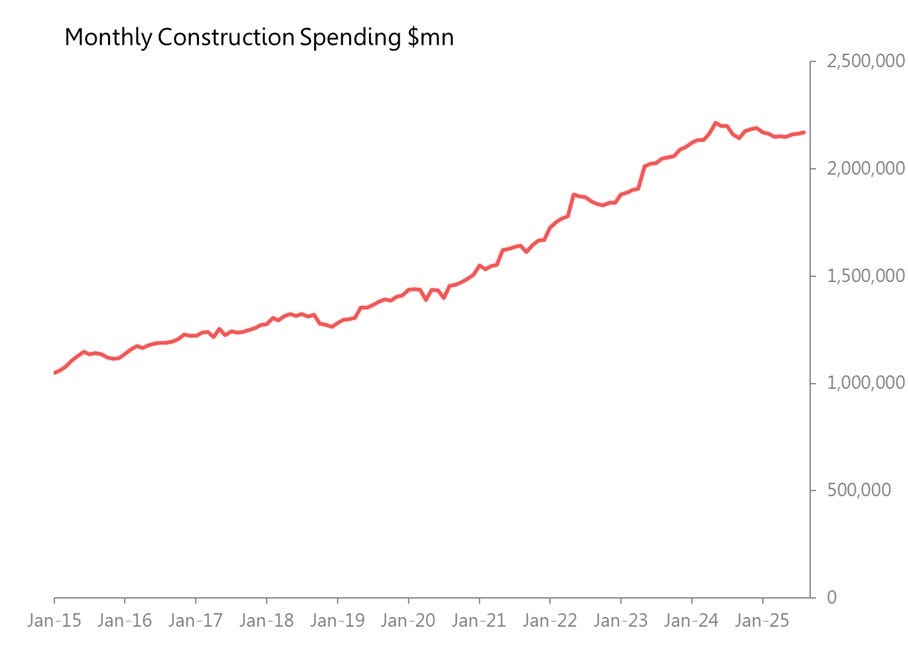

It’s important to stress that this represents no immediate emergency or change in circumstances. Nor is it a plausible trigger for recession. But when the flatlining is unchanged for years on end, it must eventually re-set expectations, and with it, labour policies and investment policies. And so the malaise will spread: industries will eventually capitulate to the reality that growth is much slower than then expected. Which seems to be what is happening now: construction spending has flatlined now since early 2024. You’ll see the same story in new housing starts and building permits - flatlined since 2022.

Why Capitulation Now?

It is this capitulation which, though it may not provoke a recession, does, I think, mark the end of a cycle. With capitulation in employment, particularly, the old cycle, the old reality, is ended, and a new one will be discovered.

This really does seem to be the message coming from labour market data. The overall tone is weak but not disastrous, and that weakness is reflecting capitulation in some sectors, offset by surprising strength in others. There’s a lot of evidence for this: the ADP’s count of private payrolls fell 32k in November, but whilst small companies were shedding employees very fast, medium and large companies were adding enthusiastically. The main victims: manufacturing, construction, info services and professional/business services. Those last two testifying both to the impact of AI, but also to the broadening of capitulation strategies.

Looking at December’s Challenger job cuts report actually makes the same point. In the 11 months to November, 1.17mn jobs were lost, and of those, 245k were owing to market/economic conditions, and 128k to restructuring, but only 9.6k were attributed to a downturn in demand. It’s not that something has changed, it is that nothing has changed. . .

None of what I have recorded is new - indeed, the conditions have remained unchanged for nearly three years. So why is the capitulation turning up now? I suggest two factors, both policy-related. First, there are two issues related to Trump’s trade policy. The first is simply the way the lack of visibility on tariffs inhibits commercial decisions throughout the economy.. Second, though, is that there are significant costs associated when existing supply chains are severed, and new ones have to be discovered and built. (This, it turned out, was the largest cost incurred by Brexit). It takes time and money and management attention for a company to maintain and recover its place in the web of commercial contracts upon which it relies. This is a long-term cost, and I expect it is not yet fully played out.

And the second factor is also political, but acute and short-term - the impact of the government shut-down, and its short-term impact on confidence. I have written about this before, and the hit showed up very hard in October, but was already considerably moderating in November.

Early Signs of Transition?

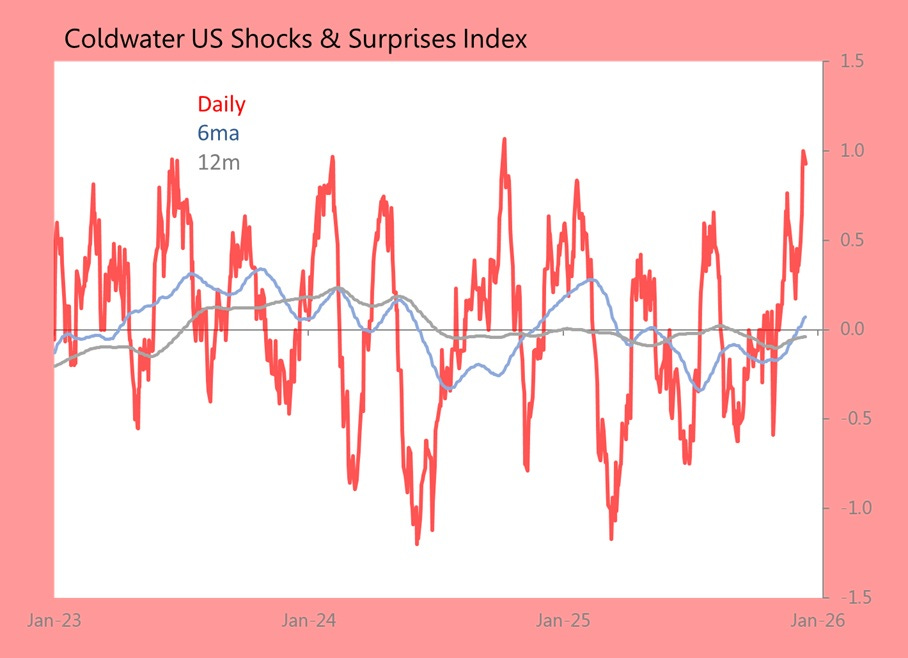

So far, so gloomy. So why do I think the US cycle isn’t ending in recession, but is rather ending and beginning in transition? There are several reasons. First, confirmation bias is everywhere, and extremely hard to escape, particularly when you are making an argument. I try to cheat it by pouring pour myself into the shocks and surprises indexes every day. Here’s what the index for the US says: economic data is coming in stronger than expected, strong enough to push the 6m trendline into positive territory for the first time since the beginning of the year. Capitulation trades are happening, but by themselves they are not enough to throw the economy into recession, seemingly.

Second, the policy-related issues likely promoting capitulation will recede. In the short term, the blow to confidence from the government shutdown have mostly already passed, according to confidence indexes. Second, the impact of tariff uncertainties and the costs of re-locating supply chains will probably already have peaked, and will recede in the medium term.

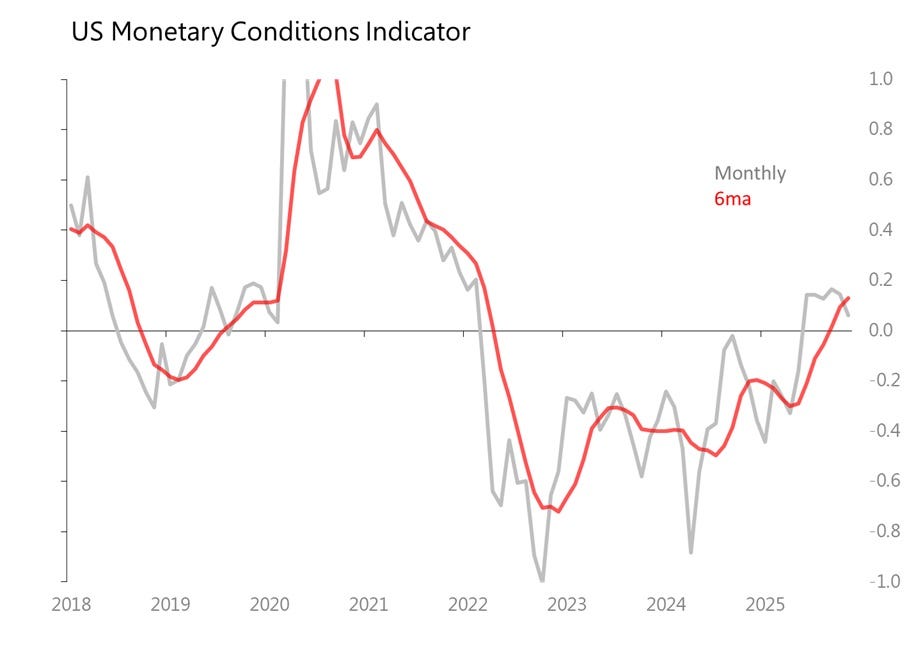

And third: If the US economy is indeed at the end of one cycle and transitioning to a new one, these are precisely the conditions in which an active monetary policy can help establish and foster the new cycle. The signs are good that monetary policy has turned supportive for the first time since, er, early 2022. This shows up not only in the Fed’s latest 25bp rate cut, but also in the decision to stop reducing its holdings of securities. It also shows up in my Monetary Conditions Indicator (includes deviations from trend in monetary aggregates, yield curve, real bond yields and FX movts vs SDR).

Conclusion and Determination

So which of my cherished beliefs do I have to ditch. Reluctantly, it is the warning from heavy truck sales. It is, I think, correctly signalling the end of the current cycle, with the ending characterised by capitulations in various sectors which have seen no significant growth since 2021/2022. Faced with volumes flat-lining for too long, restructurings are finally being made, prompted finally by the costs and uncertainties of federal policy choices. But crucially, and anomalously, it looks like this transition can be made, and is being made, without a recession being necessary, since, after all, there are no obvious signs of overwhelming ‘stock’ problems which can only be answered by a change in flows. Moreover, if a transition is being made, the birth and early years of a new cycle are being encouraged by the first sign of supportive monetary policy since 2022.