Japan's Evaporating Profits

Profits fell to record lows relative to GDP, but 2023 will discover a floor

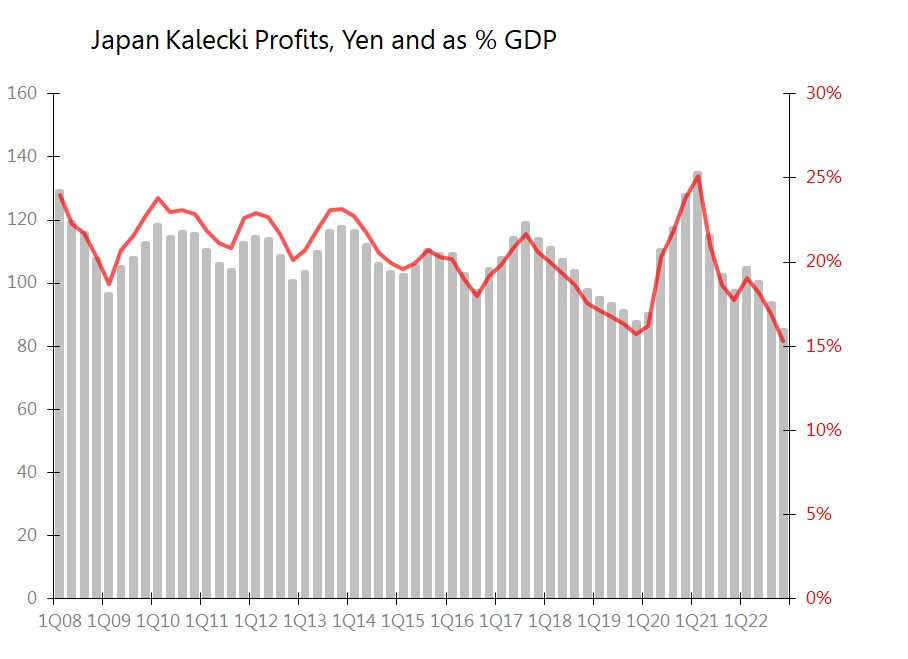

In calendar 2022, whilst Japan’s nominal GDP rose 1.3% yoy, Kalecki profits fell by 12.8% or Yn12.46tr, cutting the profits/GDP ratio to just 15.3%, the lowest this century so far. (Can it keep falling indefinitely? I asked a friend ‘What happens if Japan finally makes no profits at all. ‘Sushi gets cheaper’ he replied.)

Whilst it is difficult to expect any significant recovery in profits during 2023, we may now be near the bottom of this downward lurch. In 2023 the government deficit is likely to narrow and there’s little to be expected from net investment spending, both of which will continue to act as a drag on profits. But there should be no repeat of 2022’s terms of trade disaster, and it is reasonable to expect household dissaving to continue its recovery towards pre-covid levels. It is those - net exports and household dissaving - which should put a floor under Japan’s sagging profits.

Why the fall in 2022?

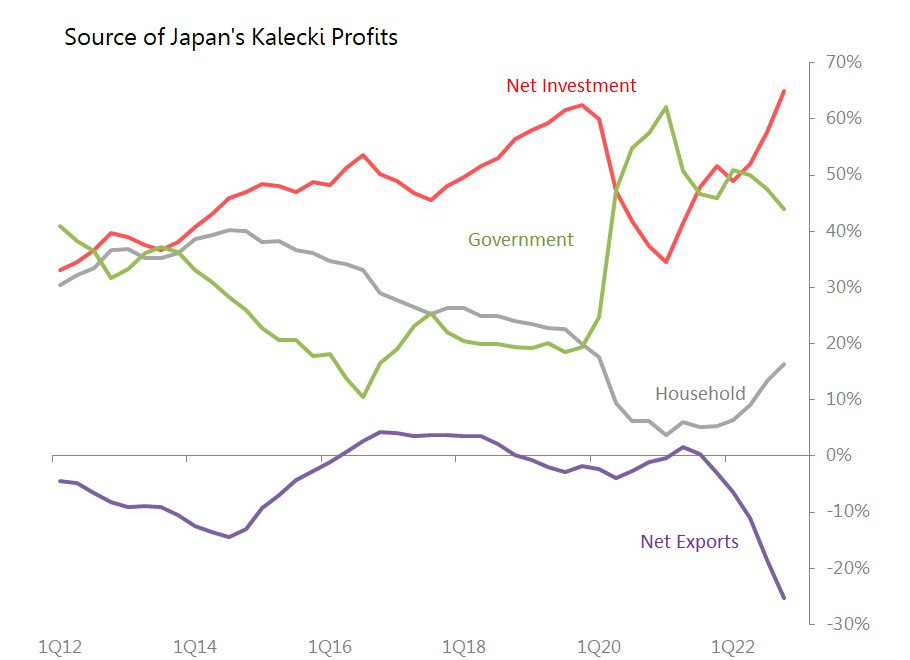

Net investment has never been more dominant as a source of Japan’s profits, accounting for a record 65% of profits in 2022. Even so, net investment rose only Yn4.9tr, or by 9.7% yoy. But even this net growth is only partly owing to the 5.1% yoy in gross fixed capital formation. What’s growing the net investment is the slowdown in depreciation growth to just 1.3% yoy as growth of estimated capital stock slowed to 1.5% yoy.

The government’s fiscal deficit remains the second highest source of profits, accounting for 43.9%. But although the government deficit remains extremely large by historic standards, at Yn37.4tr, it is no longer expanding. Rather, the 12m deficit fell by Yn7.5tr, or by 16.7% yoy in 2022, and that fiscal retrenchment is a net drag on sources of profits. One assumes that as the pandemic retreats into history’s rear-view mirror, that deficit must continue to shrink.

The collapse of Japan’s terms of trade during 2022 had a sharply negative impact on Kalecki profits. On a 12m basis, Japan’s yen export prices rose 15.8% in 2022, but import prices jumped 37.8%, resulting in a 17.2% deterioration in Japan’s terms of trade. This was echoed in a Japan’s trade position deteriorating to a Yn21.5tr deficit in 2022 from a Yn2.95tr deficit in 2021. In other words, the drag on Kalecki profits jumped Yn18.5tr, to an amount equal to 25.2% of the total. During 4Q this erosion of terms of trade was halted, and it seems unlikely that 2022’s terms of trade disaster will be repeated. This will likely provide some relief for profits during 2023.

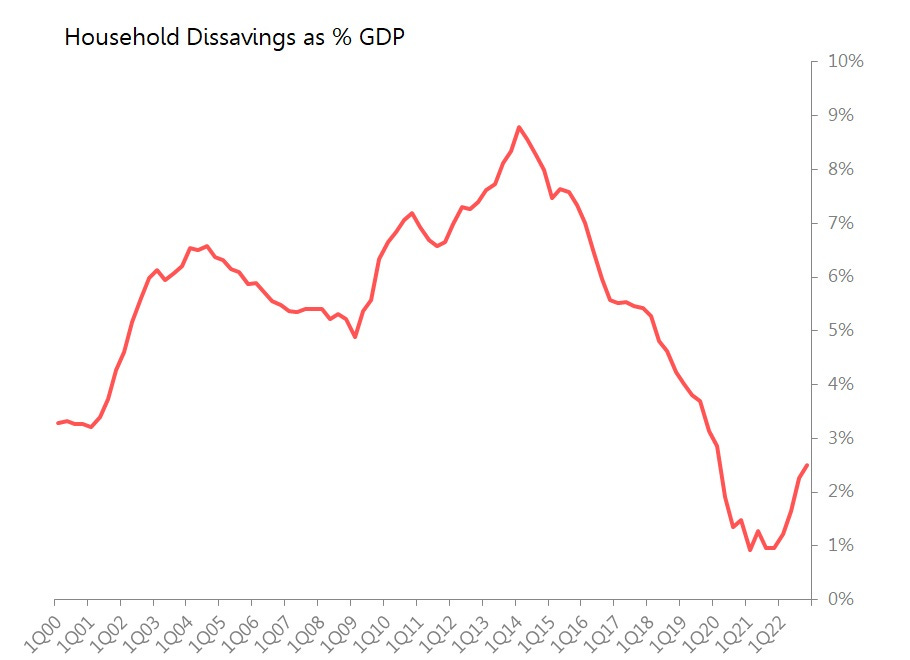

Household dissaving (the difference between private consumption and worker’s compensation) rose Yn8.6tr yoy to reach Yn13.9tr, the highest since pre-pandemic 2019. This raised its proportion of Kalecki profits by 10.9 percentage points to 16.3%. However, if there is a hope for a profits recovery, a sustained rise in household dissaving could be one of the keys. For this dissavings rate is still in the early stages of recovery from its pandemic lows. As a percentage of GDP, household dissaving rose to 2.5% of GDP in 2022, compared with an average of 5.9% of GDP during the decade before covid. A return to around 5% of GDP seems possible, likely even, over the next few years.