Chartoom Update for a De-Synchronising World

Iran War is Shuffling the Pack - updated for 14th May

We now have plenty of data from April, when the extent and implications of the Iran war were becoming clear. So this update of the Chartroom’s indexes represent an initial ‘verdict’ on how the global economy is coping.

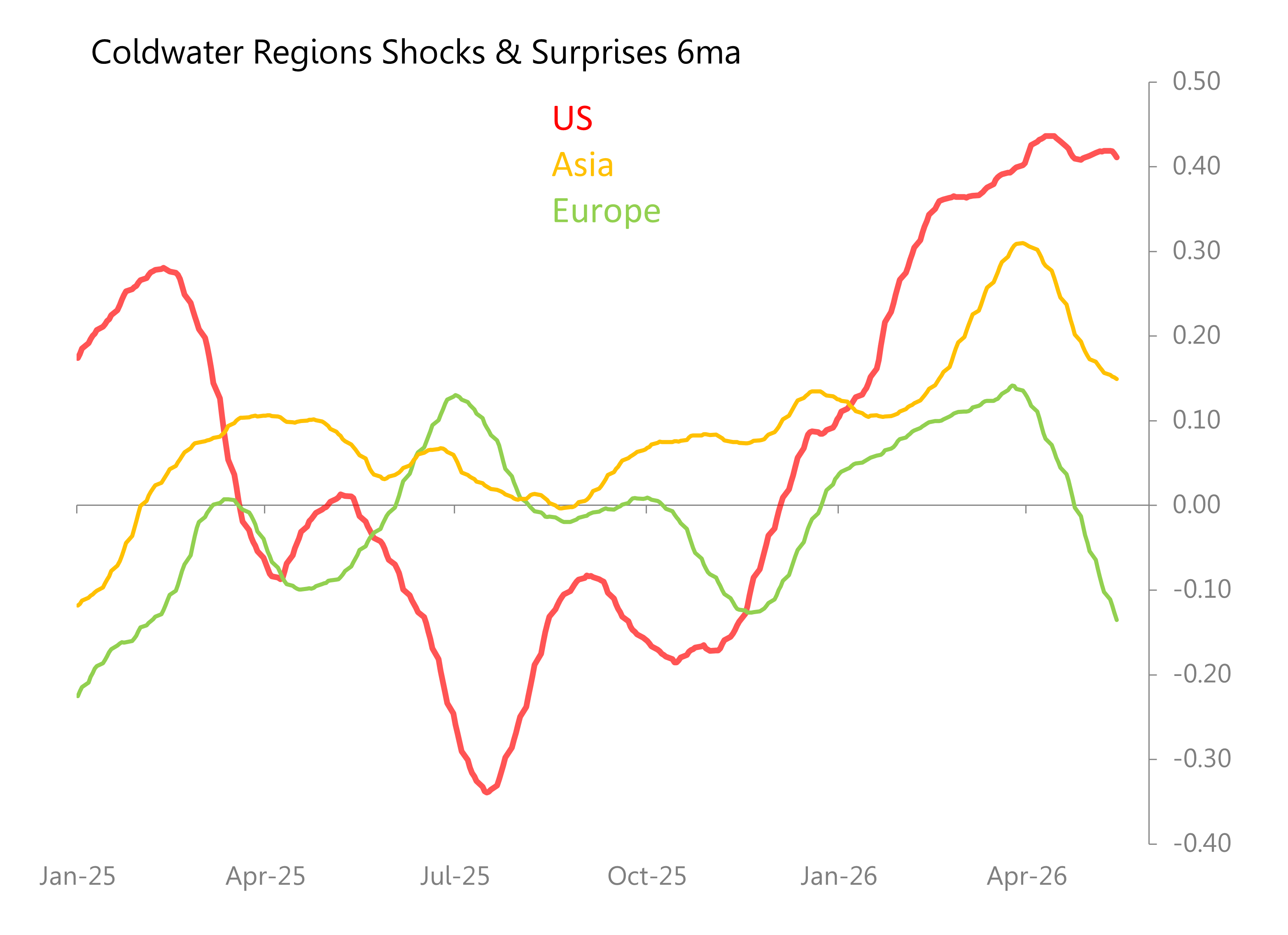

The first two charts explain a lot. The first chart shows the 6m indexes for the US, Asia, and Europe, and they record a radical de-synchronisation of the global economy. The US is taking the Iran war disruptions largely in its stride; Asia’s getting hit, but the damage partly is offset by the surge in demand for everything that is needed to build the emerging global AI & Space economy. Europe, though, is having a dreadful time: fully vulnerable to the press of oil prices, and with no substantial contribution to make to the global AI & Space economy.

The US (and to a lesser extent, China) is inventing the future, Asia is selling the spades in the oil rush, and Europe is belatedly realising experiencing the ‘slow agony’ that Mario Draghi warned about 18 months ago - this is a hostile environment for an expensive mid-tech innovation desert.

For Europe, it seems, the Iran war is the only thing going on. For much of the rest of the world, the war just complicates a lot of the other stuff that’s going on.

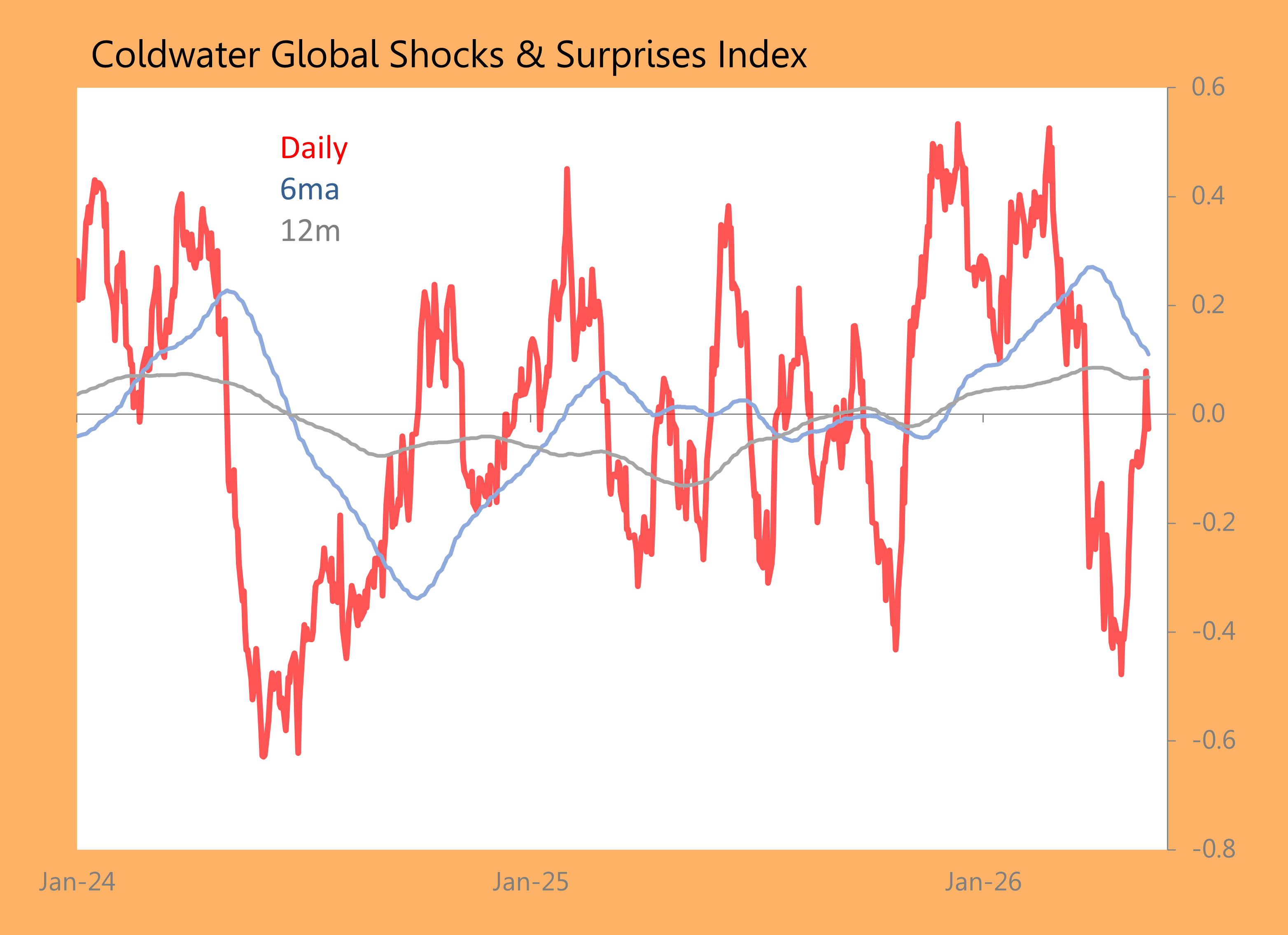

And the net result? The global shocks & surprises index is the second chart worth thinking about. It shows aggregate global data rebounding back to something near ‘normality’ after the severe initial shock of the opening salvos of the Iran war. This is probably not illusory, it reflects activity (trade, output, spending) undertaken when the Iran war was active and no longer a novel threat.

Geographically, the rest is detail: in Asia, for example Greater China continues to track sideways (Taiwan sharply positive, China and Hong Kong broadly neutral), but Japan continues to surprise, as does Asia ex-Greater China. The exception is Southeast Asia, hit hard by the oil shock and without large-enough stakes in the AI & Space emerging world.

In Europe, it is astounding, but the UK appears to be better storm-proofed than either Germany or the rest of the Eurozone. Explanations? First, a long and growing list of discovered ‘errors’ means one should be sceptical about ‘surprising’ data from the Office for National Statistics. But second, the UK’s public finances are wretchedly mis-managed by all parties and institutions, but households and corporate balance sheets are in unusually good shape. Previously, I’ve suggested the UK’s industrial economy must contain a large population of ‘tardigrades’ - animals which can survive practically anything. The UK may even discover it has a minor stake in the AI & Space economy.

More generally, the charts for global inflation and global confidence are doing exactly what you’d expect:

- the inflationary impact of the Iran war is already very clear, with inflation data showing a roughly 1.5SDs deviation from consensus/trend towards unexpectedly high inflation;

- confidence indicators, too, are showing a shocking amount of shocking - about 3SDs below consensus/trend!

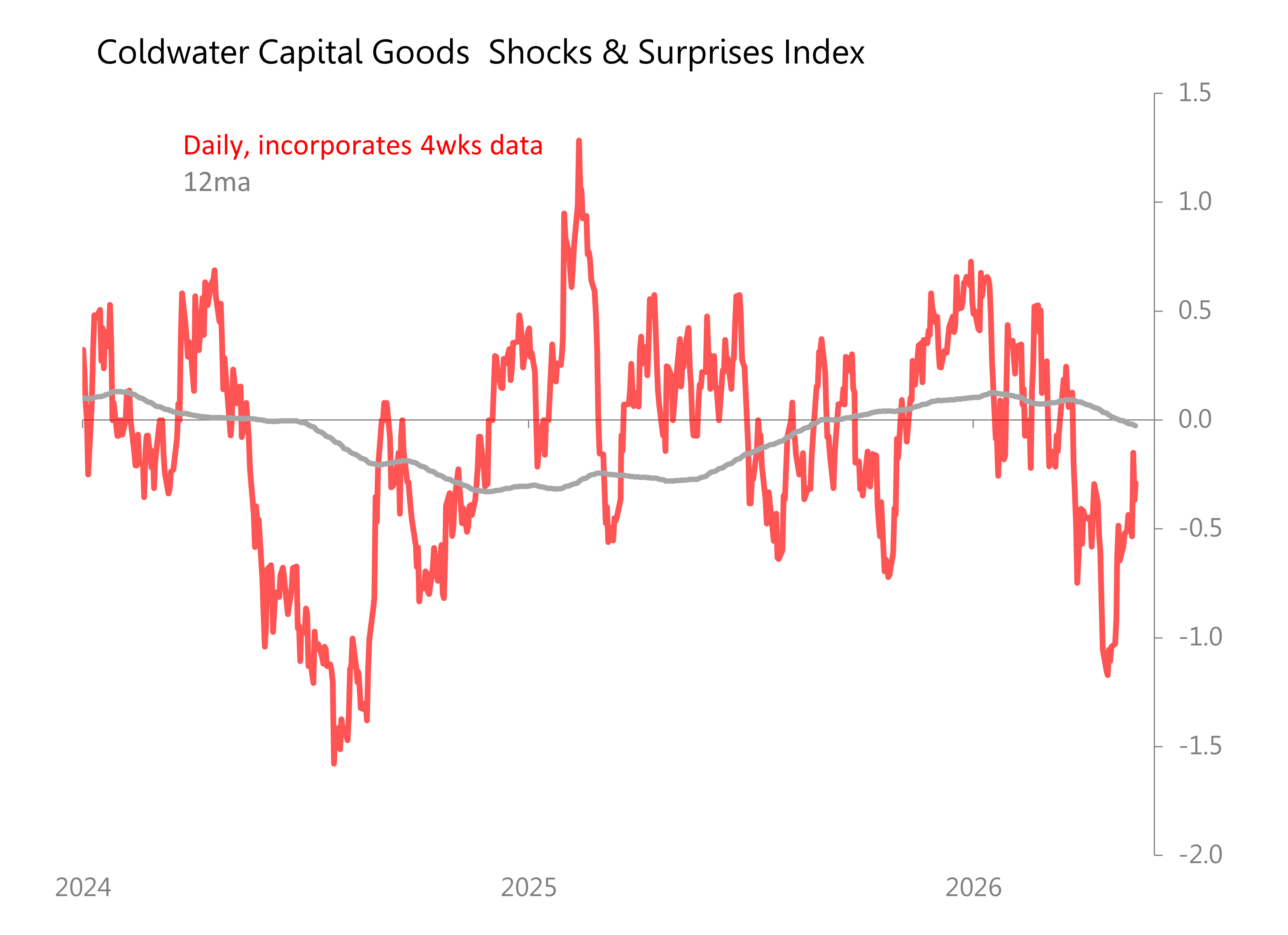

However, so far, this collapse in confidence is not mirrored by a collapse in the capital goods sector or investment plans, which after reacting strongly to the initial news of the Iran war, are now struggling back towards neutrality.

The conclusion I draw from these charts is that so far the available data does not suggest the Iran war is likely to tip the global economy into recession. That is, unless it triggers a rash of egregious strategic policy errors. What it is doing, and what it will do, is to generate economic responses and trajectories which are simply no longer synchronous between countries, or even sectors. In short, the assumptions upon which ‘globalization’ rested are being re-written in real time.